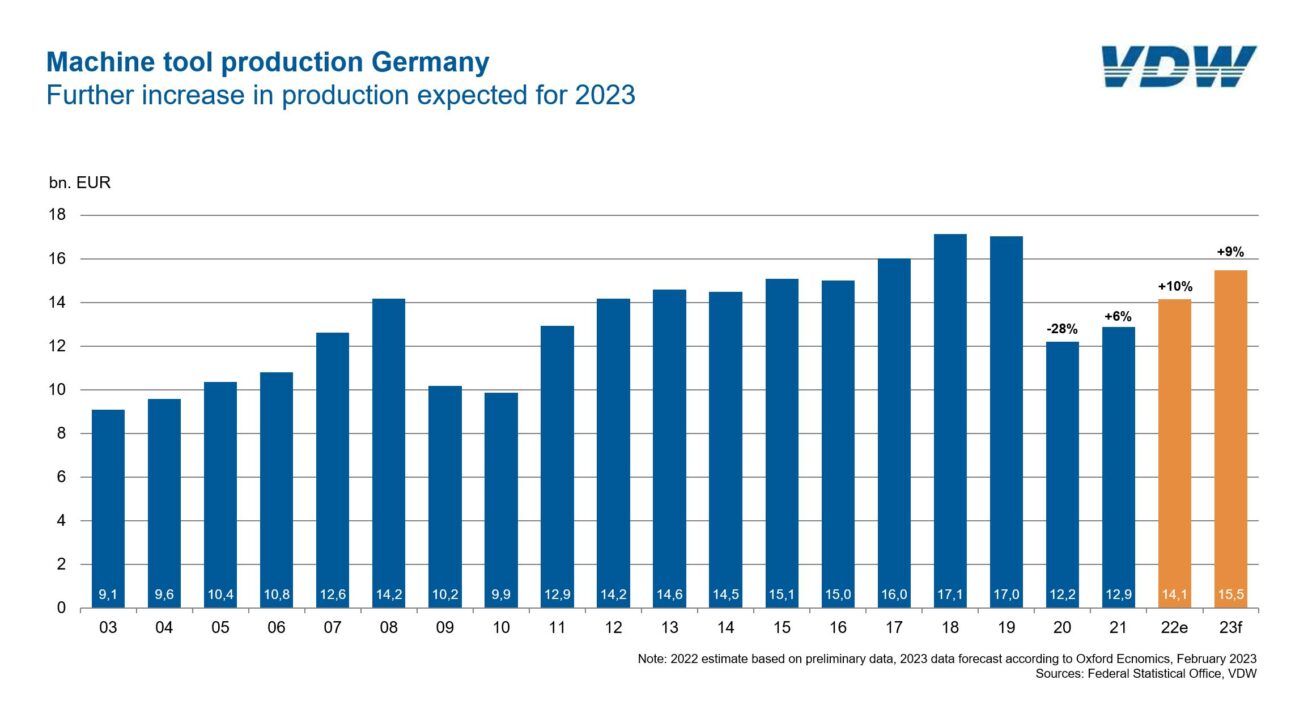

The VDW (German Machine Tool Builders’ Association) is expecting production in the machine tool industry to grow by 9 percent this year to a volume of EUR 15.5 billion. In nominal terms, this is only ten percent below the record result of 2018. At the annual press conference in Frankfurt am Main, Germany, Franz-Xaver Bernhard, Chairman of the VDW, said: “We have largely overcome the effects of the pandemic. This is reflected in the growth in production and in the order levels, which are only just short of the record result of 2018. Companies are well placed to weather any slump in orders in the first half of 2023, as suggested by the most recent figures,” explains Bernhard.

Capacity utilization is also rising steadily, having returned to 91.1 percent in January. The latest VDMA flash survey conducted at the beginning of December shows that 45 percent of machine tool manufacturers are cautiously optimistic about the current year.

Inflaction has peaked

In macroeconomic terms, the forecast is underpinned by the assumption that inflation has peaked. Energy and commodity prices have now begun to fall again. The lifting of Covid restrictions in China, the largest market, will stimulate business. Other Asian countries such as India and the ASEAN region are also contributing to growth. Global investment is rising for the third year in succession, albeit less dynamically than in the previous two years. International machine tool consumption is benefitting from this.

In Germany, too, capital expenditure is expected to rise again after three sluggish years. Here, the automotive industry in particular had reined in its spending after the chip shortage made it impossible to produce vehicles. “The machine tool industry has taken advantage of the transformation process among automotive manufacturers and redoubled its efforts to diversify its customer structure. According to our customer structure survey, the share of the automotive sector fell from almost 43 percent in 2019 to around 31 percent in 2021,” explains the VDW chairman. Making gains, by contrast, are engineering and the manufacture of metal products.

Double-digit growth in 2022

According to VDW estimates, machine tool production grew by ten percent last year, three points more than had been expected in the fall. This corresponds to a real increase of 3 percent and a volume of around EUR 14.1 billion. “At last, more machines can now be completed and delivered, because the supply situation for many metal components has improved,” points out Bernhard. However, electronic component supplies remain tight.

Following a weak previous year, domestic sales grew by 16 percent, more than twice as fast as exports at only 7 percent. Europe came last within the Triad, at minus 3 percent. Eastern Europe performed particularly weakly because trade with Russia has largely collapsed. Cumulatively, German shipments have declined by nearly 80 percent since 2018. Italy has performed exceptionally strongly in the past two years, driven by a substantial subsidy policy for the purchase of machinery. Exports to Asia rose by 11 percent.

There was strong growth in exports to Thailand, India, Japan and South Korea in particular. China was the main driver the year before. In 2022, the zero Covid policy made machine deliveries more challenging. Some exports were replaced by local production. Finally, the Americas were the main driving force with a 24 percent increase, driven by Brazil, the USA and Mexico. As the second largest market, the USA is gaining in importance and, accounting for an export share of 14.7 percent, is closing in on China, at 18.7 percent.

The total workforce was put at 65,400 in December 2022 in establishments with more than 50 employees. That was 2 per cent higher than in the previous year. There has been a 13 percent reduction in the workforce since the pandemic began in 2019. Production decreased by 17 percent in the same period. This is attributable not only to the pandemic, but also to the transformation process which automotive customers are undergoing.

Better training and development for skilled workers

In a survey, 31 percent of machine tool manufacturers reported a new and serious challenge that is becoming increasingly acute. For a further 50 percent, it is a problem they are already contending with. This is the severe shortage of skilled workers.

“The shortage of skilled workers is likely to remain an ongoing issue because of its structural cause in the form of demographic change in Germany. The figures for the engineering sector as a whole confirm how precarious the situation is,” says VDW Chairman Bernhard.

The number of job openings in engineering is rising much faster relative to the overall increase in personnel: 20 versus 1.3 percent. Just over half of all engineering companies are planning to take on new staff. However, according to calculations by the German Economic Institute, the supply of skilled workers in STEM fields will at best only cover half of the industry’s needs in the coming years. The Federal Employment Agency reports major shortages in the following occupational groups at present: mechatronics technicians, automation technology, metal cutting, mechanical and industrial engineering, and electrical engineering. In the 2021/2022 training year, more than 11,000 of the 97,000 training places offered in engineering-related occupations remained unfilled.

Source: https://vdw.de/

{kind=link}